Some Known Details About Mortgage Investment Corporation

Some Known Details About Mortgage Investment Corporation

Blog Article

Unknown Facts About Mortgage Investment Corporation

Table of ContentsThe Main Principles Of Mortgage Investment Corporation How Mortgage Investment Corporation can Save You Time, Stress, and Money.Getting My Mortgage Investment Corporation To WorkThe Only Guide to Mortgage Investment CorporationHow Mortgage Investment Corporation can Save You Time, Stress, and Money.The 7-Second Trick For Mortgage Investment Corporation

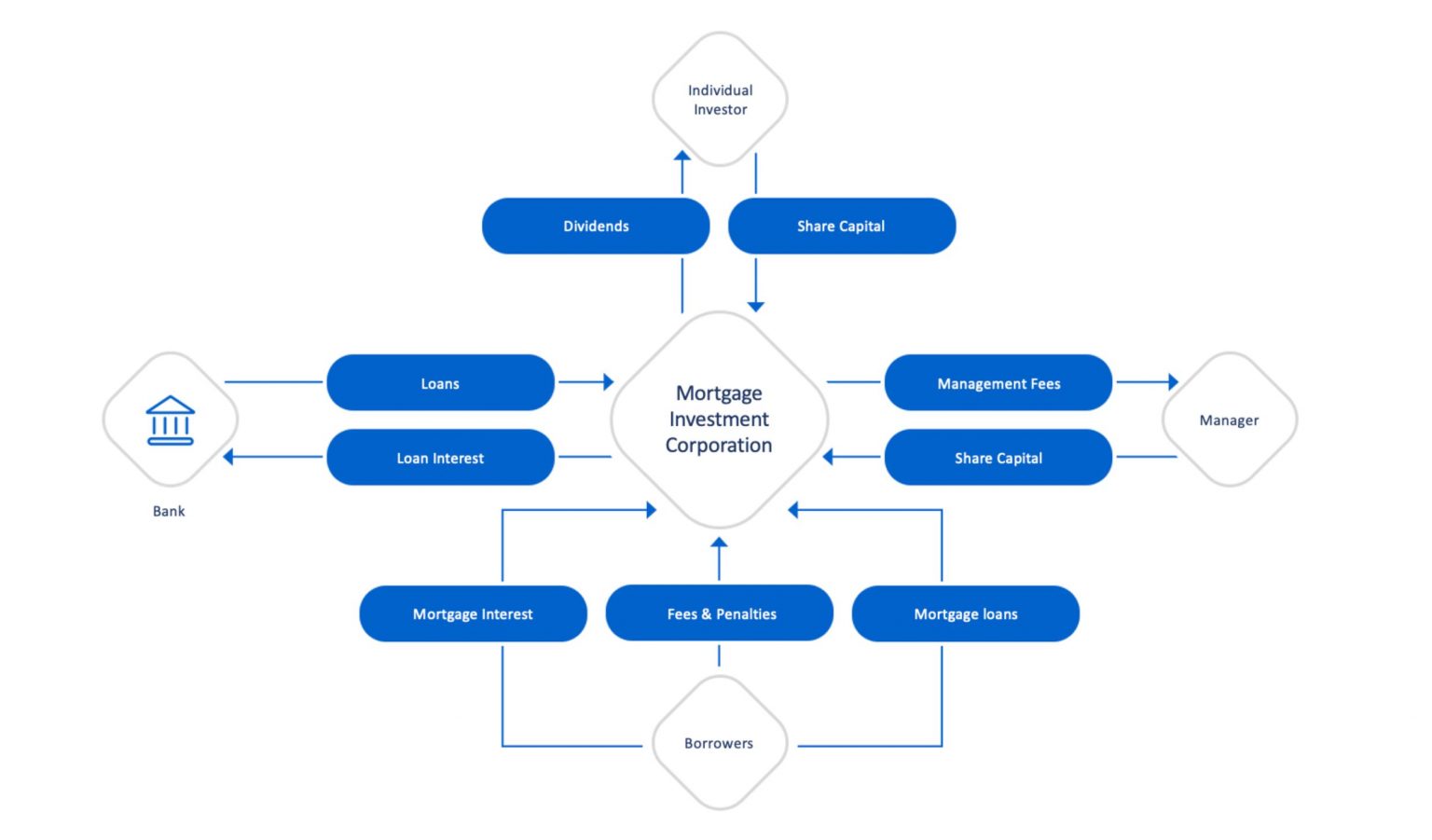

Mortgage prices from a MIC is usually around 9% to 12% Not poor eh? Management charges and various other prices connected with running the MIC consume away about 2% to 4% of the complete income, so before tax obligation, depending on the mix of mortgagesThere are lots of MICs across the country to pick from.

The Basic Principles Of Mortgage Investment Corporation

What is the mix in between 1st and Second mortgages? What is the dimension of the MIC fund? This information can be found in the offering memorandum which is the MIC matching of a mutual fund program.

Just how to leave the financial investment and exist any kind of redemption fees? Some MICs have limitations on the withdrawal procedure. Ask the firm for information. To make things simple I recommend maintaining your findings organized for comparison purposes later, such as this for instance. The MIC I have actually picked is Antrim Investments.

and mostly concentrate on property home mortgages and tiny commercial finances. Below's a check out Antrim's historic returns. I really feel like the property allocation, expected returns, and diversification of property for this MIC suit my risk tolerance and investment needs so that's why I chose this one. Over the last 3 years the annual return has been 7.17% to investors, so I will assume as the expected return on my new $10,000 MIC investment for the time being.

Indicators on Mortgage Investment Corporation You Need To Know

A popular trustee in B.C. and Alberta is Canadian Western Trust. To open up an account with Canadian Western we simply fill in an application which can be located on its web site. Next we give directions to our trustee to buy shares of the MIC we desire. Here's my instance.

We'll also need to mail a cheque to the trustee which will certainly represent our initial down payment. Regarding 2 weeks later on we must see cash in our brand-new trust account There is a yearly cost to hold a TFSA account with Canadian Western, and a $100 transaction charge to make any kind of buy or sell orders.

MICs aren't all that and a bag of potato chips There are genuine dangers as well. The majority investigate this site of MICs maintain a margin of security by keeping an affordable loan to value ratio.

The Only Guide for Mortgage Investment Corporation

I have just bought 2 added MIC funds. This time around, publicly traded ones on the Toronto Stock Market. [/modify]

This constant circulation of cash makes certain that lending institutions constantly have funds to offer, offering even more people the chance to accomplish homeownership. Financier guidelines can also ensure the security of the home mortgage market.

After the loan provider offers the loan to a mortgage financier, the lending institution can make use of the funds it receives to make more finances. Mortgage Investment Corporation. Giving the funds for loan providers to develop even more fundings, investors are vital since they set standards that play a role in what kinds of fundings you can get.

The Ultimate Guide To Mortgage Investment Corporation

As property owners settle their home mortgages, the payments are gathered and dispersed to the private investors who got the mortgage-backed securities. Unlike government companies, Fannie Mae and Freddie Mac do not insure financings. This indicates the personal capitalists aren't ensured settlement if customers do not make their finance payments. Considering that the investors aren't secured, conforming fundings have more stringent guidelines for establishing whether a debtor certifies or not.

Since there is more threat with a larger home loan amount, jumbo lendings tend to have more stringent consumer qualification requirements. Investors likewise handle them in a different way. Traditional jumbo loans are generally as well big to be backed by Fannie Mae or Freddie Mac. Rather, navigate to this website they're offered straight from lending institutions to personal capitalists, without including a government-sponsored enterprise.

These companies will certainly package the fundings and market them to personal capitalists on the secondary market. After you close the lending, your lending institution may offer your financing to a financier, yet this generally does not change anything for you. You would still make settlements to the lender, or to the home loan servicer that manages your mortgage repayments.

After the lending institution sells the finance to a home loan financier, the lending institution can use the funds it gets to make even more financings. Providing the funds for lenders to produce even more finances, investors are essential since they establish standards that play a duty in what types of car loans you can obtain.

The Main Principles Of Mortgage Investment Corporation

As home owners pay off their home loans, the payments are accumulated and distributed to the personal capitalists who acquired the mortgage-backed safety and securities. Since the financiers aren't protected, adhering lendings have more stringent guidelines for determining whether a debtor qualifies or not.

Department of Veterans Affairs establishes standards for VA fundings. The U.S. Division of Farming (USDA) sets guidelines for USDA finances. The Government National Mortgage Organization, or Ginnie Mae, supervises federal government mortgage programs and insures government-backed finances, safeguarding private investors in case debtors default on their lendings. Big lendings are home loans that exceed adhering financing limits. Due to the fact that there is more risk with a larger home mortgage amount, jumbo finances tend to have stricter debtor qualification needs. Financiers additionally handle them in a different way. Standard big lendings are normally also large to be backed by Fannie Mae or Freddie Mac. Instead, important site they're sold directly from lending institutions to exclusive capitalists, without entailing a government-sponsored enterprise.

These firms will certainly package the lendings and market them to personal financiers on the additional market. After you close the funding, your lender might offer your finance to a capitalist, however this normally doesn't change anything for you. You would still pay to the loan provider, or to the mortgage servicer that handles your home mortgage repayments.

Report this page